for hardship withdrawals in 2025")

Marklyn Johnson drove to the grocery store in March 2025 with her boyfriend and 5-month-old son. They needed groceries, and welcomed a warm indoor diversion on a cold Connecticut winter day.

As they were checking out at the register, Johnson looked out the window and noticed her car was gone.

“I didn’t know what to do,” says Johnson. “I didn’t know what to say, I didn’t know who to call.”

Turns out, according to Johnson’s legal complaint in Hartford’s superior court, the used car dealership that sold her the vehicle two months earlier had decided to repossess it at that very inopportune time — even though she hadn’t missed a single payment.

Unfortunately, Johnson’s story is one of many. Bankrate has interviewed consumer protection lawyers across five states who are representing clients in similar, ongoing cases. One lawyer called them “rampant.” Some aren’t simple repossessions either, especially when the dealer or its auto financing partner involves the police by reporting a car as stolen if the consumer doesn’t return it promptly.

Sparky Abraham, a California-based attorney, says one of his clients never expected her car repossession story to end in handcuffs.

“I’m not at a place with the latest [case] yet that I can say a lot,” says Abraham, “but I will say, [my client] took a video of herself getting arrested, and there are guns pointed in her face, like for buying a car, you know?”

Like that woman, what happened to Johnson started out simply as “yo-yo financing”: Her dealer guaranteed loan approval and, five days after the sale was “finalized,” started texting and calling her to say it fell through. She was given a choice before the repossession: Either return the car or succumb to less attractive loan terms.

Most consumers, when confronted, want the car they’ve already started driving and “eat the difference and sign a new contract,” says lawyer Bryce Bell, a consumer attorney in Kansas City. Other consumers simply aren’t aware of their legal rights. That means only a fraction of these bait-and-switch cases are actually litigated.

As part of Bankrate’s ongoing effort to shed light on predatory financial practices, yo-yo financing seems worthy of spotlighting.

Johnson ‘wasn’t prepared for what was to happen next’

Johnson, 23, and her now-14-month-old son needed a car for the same reasons we all need wheels: to get to and from doctor’s appointments, work and so on. So, when she tired of borrowing her parents’ car, Johnson sought out something affordable, zeroing in on a 2017 Acura ILX listed by Hartford Auto for $13,999. The used car dealer claimed to offer “guaranteed” approval, according to the legal complaint, but to seal the deal, asked Johnson to increase her initial down payment from $1,500 to $3,200.

“Knowing that it was in my name, that I just bought it, that it was ‘new,’ there was nothing wrong with it — I was so excited,” says Johnson, who’s currently pursuing a nursing career. “And then, knowing that my baby had a car, everything was just falling into place.”

Things fell apart about five days after she drove the Acura off the lot. Texts and calls from the dealer saying “she needed to sign new financing documents because there were issues with [financing partner] Winthrop Financial accepting the loan,” the complaint reads.

“I’m not going to lie… my heart did drop,” Johnson recalls. “I already signed the contract, I already did what I needed to do… I wasn’t prepared for what was to happen next.”

Related: Car repossessions are up 43%. Here’s what to do if it happens to you

Two months later, in the grocery store parking lot, Johnson found herself without a car altogether and the immediate concern of how to get home. She remembers an Uber driver allowing her toddler to get into the car without the base for his car seat.

It was left in the Acura that had just been towed away.

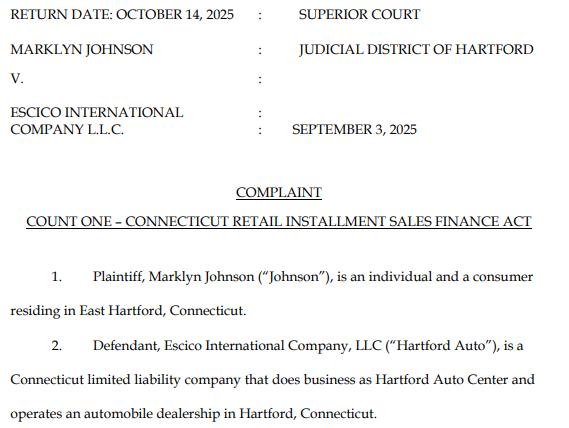

Read Johnson’s full legal complaint.

Yo-yo financing made possible by one-sided auto purchase contracts

Yo-yo financing is what it sounds like. Imagine yourself experiencing the high of driving off the lot and the low of being summoned back, perhaps to make a bigger down payment or face a higher interest rate. In the days between, you might have shown off your new ride to family and friends, perhaps upended your budget to make the math work.

“You’re really invested, and it’s hard for people then to say, ‘no, I’m not going to pay another $2,000 down or whatever it is the [dealer’s] asking,” says National Consumer Law Center (NCLC) senior attorney John Van Alst. “Sometimes, in the most egregious cases, this is done as a technique: [Dealers] haven’t even checked with other finance companies they’re trying to assign the retail installment sales contract to — they’re just doing this as a way to get you to agree to more onerous terms.”

Believe it or not, yo-yo financing in and of itself (before the renegotiation or repossession) is perfectly legal, as each state gives dealers a certain number of days to finalize financing after the buyer has signed their paperwork. It’s four days in Washington, for instance, but 10 in California. If the dealer can’t secure financing, it can cancel the contract within that window.

That’s despite the efforts of the NCLC and the National Association of Consumer Advocates (NACA) to lobby the FTC for something simple and uniform.

“It doesn’t even have to be highly regulated,” agrees NACA senior policy director Christine Hines. “It just means the contract is a final contract — there shouldn’t be any conditions on it that [harm] a consumer… because the dealer doesn’t know how to conduct a transaction.”

The dealers sure want [transactions] to be final for the consumer — they don’t want the consumer to be able to change their mind later, but they love trying to enable the dealer to change their mind after the fact. It’s a little bit of what’s good for the goose is good for the gander.

— John W. Van Alst, NCLC senior attorney

Also known as bushing or spot-delivery scams, yo-yo financing can be even more troublesome for buyers who financed a new car by trading in their older model. In such cases, a dealer might sell your trade-in before it calls you back to renegotiate your loan.

Bankrate has reported on the fact that car dealers have been exempt from federal oversight since the dawn of the Consumer Financial Protection Bureau — the CFPB’s recent sidelining has little do with it. There’s also the fact that where you live determines how protected you might be from auto retail scams: Regulators in your state may be more motivated than their peers elsewhere.

Related: Predatory auto loans are legal, and some dealers are offering them to unknowing consumers

But another unfortunate reality is that yo-yo financing appears to occur nationwide. And it’s just as befuddling for the professionals who litigate these cases everyday. Bell, the Missouri-based lawyer, wonders why buying a car seems to be the only transaction where the seller can change its mind after the contract’s been signed.

“If you’re an honest dealership, and an honest business, why wouldn’t you want that deal finalized for the consumer?” Bell asks.

Like other matters in life, follow the incentives, Bell adds. If a car salesman is incentivized, perhaps by commissions, to get a buyer to leave the lot inside of a car, they might push the envelope to do it. And without federal regulation (or enforcement), dealers are free to let these mistakes (or sometimes malicious behavior) happen.

Eighteen state attorneys general wrote to the FTC in 2022 asking it to “go farther to prevent this unfair and deceptive practice.” The FTC’s ill-fated attempts to solve for yo-yo financing and other auto fraud was beaten back by the courts in January 2024.

How dealers handle failed yo-yo financing cases like Johnson’s — and how law enforcement handles the fallout — also depends on where you live. But the police precinct might matter more than your state. Abraham, the California lawyer, says he has worked on a pair of southern California cases involving police departments in close proximity: One department treated it as a civil dispute, another acted as if it was a criminal matter and arrested the car buyer.

“These are neighboring jurisdictions, right?” says Abraham. “This is Anaheim Police Department, Pomona Police Department. This is LAPD and Beverly Hills PD, right?”

And if the dealership reports a car as stolen, perhaps because they can’t find it as easily as Hartford Auto found Johnson’s Acura at Aldi’s, the value of the car could mean the buyer faces felony-level charges.

What to do if you find yourself in Johnson’s shoes

Get everything in writing. That’s the go-to advice of the consumer protection lawyers interviewed by Bankrate. Then you have a record of what the dealer is doing and when, and can prove that yo-yo financing, while legal, led to something that isn’t.

Your best defenses are to read and retain all documents. Be especially wary of conditional delivery agreements. Instead of driving off the lot right away, make sure all aspects of the transaction are finalized, even if that means waiting a few days to pick up the car.

— Ted Rossman, Bankrate’s senior industry analyst

In Johnson’s case, her complaint alleges that Hartford Auto violated Connecticut statutes for not providing, for example, pre- or post-repossession notices, including her 60-day right to retrieve her personal belongings (such as the base for her son’s car seat). It similarly didn’t share its intent to resell the Acura (which it did last August). The complaint also says Hartford Auto violated the Connecticut Unfair Trade Practices Act for, among other things, misrepresenting that Johnson would be — and was — approved for financing. While she never recovered her $3,200 down payment, she’s now seeking more than $15,000 in damages, plus attorney fees.

Seeking legal help is another smart move, particularly if you need help understanding your rights — just be mindful that you might not always get a reassuring response. Abraham, for instance, has received calls from prospective clients who relay a commonly-heard threat from a dealership: Bring the car back, or we’ll call the police.

“My advice is, ‘Look, it [might be] illegal for them to do that. They might still do it, and if they do it, you can call me, and maybe you’ll have a case, and you can sue them for damages. But your life would probably just be better if you… consider just [returning] the car,’” he says.

It’s also wise to submit a complaint to the CFPB and the FTC (even if it goes unheard) and your state’s consumer protection office. At the very least, it creates a record of your experience that could result in broader, more meaningful change.

As for Johnson, her first car-buying experience certainly left a “bad impression.” If she had a redo, she’d do her best to budget and save up for a car, avoiding borrowing — and car dealer tricks — altogether.

“If I could think back then,” she says, “I probably would just wait, feel like a burden [to my parents] as long as I had to, in order to save up for a car that I could buy outright, that I could call mine at the end of the day.”

Why we ask for feedback

Your feedback helps us improve our content and services. It takes less than a minute to

complete.

Your responses are anonymous and will only be used for improving our website.

Help us improve our content

Read the full article here