Andy Challenger is the person businesses call when it’s time to let workers go. And for the past year and a half, his phone hasn’t stopped ringing.

A third-generation outplacement consultant at Challenger, Gray & Christmas — the firm his grandfather founded in the 1960s after his own layoff — Challenger has heard a variety of reasons over the past few months for trimming headcount. Companies looking to cut staff after the pandemic-era hiring boom. Executives debating how to integrate artificial intelligence. Businesses worrying about eating the cost of higher tariffs. Firms tightening their belts in a slowing economy.

As economic data continued to suggest a shockingly resilient labor market, his workload told a different story.

For the past four or five months, things have been worse than the numbers showed. There has been an increase in layoffs, and from what I know, there will be continued layoffs for the next few months.

— Andy Challenger, chief revenue officer at outplacement firm Challenger, Gray & Christmas

Anyone who has watched a friend lose work, seen a “Now Hiring” sign quietly come down, scrolled through LinkedIn profiles marked “#OpenToWork” or worried about how far your own paycheck will stretch, knows what Challenger is talking about. Economic reports can tell one story; your reality often tells another.

For much of the past few years, Americans have been told the job market was strong. The numbers showed solid hiring and low unemployment. Economists have said it’s propped up the entire economy, fueling consumer spending that keeps surprising forecasters.

But for many, that story has never quite matched what was happening at their kitchen tables. More than 2 in 5 workers (43 percent) didn’t receive a pay increase at all over the past 12 months, the highest in four years and a sign of a slowing job market, according to Bankrate’s new Pay Raise Survey. A rising share of Americans in the labor force (42 percent in 2025 from 36 percent in 2024) also say they aren’t confident they’ll find a better-paying job or get a pay raise at their current position over the next 12 months.

More workers than ever say their pay isn’t keeping pace with inflation

A record 62% say their income hasn’t kept up with their expenses, climbing from 55% in 2022.

Read more

Economists are realizing that Americans were right all along

The data may finally be starting to reflect Americans’ experiences. Hiring over the past four months has flatlined. Recent revisions from the Bureau of Labor Statistics show the economy added nearly a million fewer jobs — 911,000 — than previously reported between March 2024 and March 2025. All of it’s adding to signs that Americans may have gotten it right, economists say.

The data did catch up to what people were saying. In hindsight, it’s very clear the job market has been frozen for longer than we realized. People who were trying to say, ‘this is not my experience’ were vindicated when the final revised data was coming out.

— Heather Long, chief economist at Navy Federal Credit Union

The numbers, though, still might not be telling the full story. The U.S. economy grew by the fastest pace in almost two years last quarter, but that might be because upper-income Americans are propping up spending. The top 10 percent of Americans now account for nearly half of consumer spending, up from 35 percent in the early 1990s, according to Moody’s Analytics.

Meanwhile, artificial intelligence is juicing up the economy. Business investment in intellectual property contributed just over one-fifth of recent economic growth in the second quarter of this year, data from the Department of Commerce shows.

The disconnect can give Americans the perception that they’re struggling alone. Over 2 in 5 (43 percent) U.S. adults say money negatively affects their mental health, above things like their health and relationships or even politics and world news, according to Bankrate’s Money and Mental Health Survey.

Those Americans are also nearly three times more likely to have paid a bill late in the last month, the survey found.

“If everyone is struggling, well, then it’s a systemic breakdown. If I’m the one struggling, whether that’s true or not, well, there’s something wrong with me,” says Nate Astle, a certified financial therapist and the founder of the Financial Therapy Clinical Institute. “My cynicism for the media or the stats I’m hearing and my distrust of institutions grows even wider because this isn’t even close to my experience.”

Those discrepancies also make it harder for policymakers to prescribe the right medicine. Federal Reserve officials cut interest rates at their September meeting to give the labor market more support, but they’ve been cautious about moving too quickly, fearful that they could worsen inflation. Keeping rates high for too long, though, could weaken the job market even more.

“In this moment in particular, there is a greater need to understand what’s going on at different income levels and for different populations,” Long says. “For the bottom 80 percent, we can see it in their spending habits. This is not a boom time for them. This is very much a back to the paycheck-to-paycheck lifestyle. The real concern is, when does it go from paycheck to paycheck to starting to miss bills?”

The job market might not be getting much better, says this small business owner

Chris Taylor has a foot in both worlds. A trained economist turned small business owner, he co-owns Manhattan’s oldest chocolate house, Li-Lac Chocolates, with six locations around New York City. But Taylor doesn’t need data to confirm that the job market is slowing. He sees it on the ground.

“We are getting seriously qualified candidates that six months ago wouldn’t be bothered to talk to us,” he says. “The Fed sets interest rates based on whatever magic formulas they have, and then you ride the wave. You can’t control the waves that you ride, but I see huge labor market weakness, and I see huge pricing pressure on the retail side.”

Taylor doesn’t foresee the picture changing much anytime soon. Li-Lac’s costs have stayed manageable thanks to year-ahead contracts for chocolate and gift boxes, but they’ll have to place another order after the holidays. If the Supreme Court upholds President Donald Trump’s steep ‘reciprocal tariffs,’ Taylor expects a major jump in expenses. He’s searched for U.S. suppliers with the same quality and reliability but hasn’t found any.

He doesn’t know if he can pass those higher costs along to his customers, either. Taylor first noticed a slump in sales back in August, which he mainly attributes to weaker tourism.

To stay afloat, he’s implementing a hiring freeze for his 70 permanent employees and rethinking raises, after previously boosting pay an average of 25 percent over the past three years.

“If my costs increase on raw materials, I have to cut it somewhere, and I have to cut it in labor,” he says. “I like to give good raises. It’s cheaper to pay good people well than it is to pay mediocre wages.”

Like many business owners, Taylor isn’t planning layoffs yet, but he’s bracing for the possibility. Chocolate prices have already quadrupled in four years. Every week another small chocolatier calls him looking to sell.

“The biggest enemy of business is uncertainty. You can give me any bad news as long as it’s something I can plan around. It’s the uncertainty that hurts you. Every business owner is pulling back on spending, whether it’s investment or payroll or whatever. The damage is already done.”

— Chris Taylor, co-owner of Li-Lac Chocolates

A tough economy forced this small business owner to close up shop

Hidden behind the numbers is also heartbreak. Nicole Panettieri had just finished teaching college students how to create a small business proposal when she realized it was time to say goodbye to one of her own.

Panettieri owns two boutiques in Astoria, Queens: The Brass Owl, a women’s apparel and accessories shop that she opened in 2014, and The Tiny Owl, a toy and children’s store she launched after the pandemic.

But her debts were piling up, her rent was rising faster than her sales and tariffs had pushed The Tiny Owl’s costs up about 15 to 20 percent. When a Target opened around the corner, foot traffic died.

At the end of October, she’ll close The Tiny Owl for good, laying off two employees and cutting hours for three more.

On the subway ride home from class, she cried for the first time.

“The day I told my team that it was gonna happen, it felt the most real,” she says. “We all fought really hard to make it work. It feels like we all failed. There were too many obstacles for a business that’s only three years old.”

Motherhood and the experience of navigating city life with a newborn during the pandemic, changing diapers on park benches, inspired her to open the kids’ store. She vowed to create a safe space for families that she never had. Toys quickly became her bestseller, making up more than half of her business. She had hopes of eventually expanding. Then, tariffs hit.

Prices jumped almost overnight. Vendors canceled shipments or delivered goods with duties higher than the cost of the order. She had no choice but to pass the increases on to customers. All the while, she watched as passersby outside carried shopping bags from her lower-priced national competitors around the neighborhood.

“Once prices are up, they’re up,” she says. “No one goes backwards.”

Costs at her other shop have fared better, but sales are still down about 12 percent from last year. She’s paused hiring, cut hours heading into the holidays and skipped raises for the first time in 11 years. To save The Brass Owl from the same fate, she launched a GoFundMe that’s already raised nearly half its goal.

A year ago, she dreamed of opening a third store. She lives for the little moments, like watching kids around the neighborhood grow up. Once, a shopper told her she’d bought shoes from Panettieri’s store for her first date and was now getting engaged. Now, she’s debating whether to sell or close in a few years.

“You’re part of people’s lives, and I have the honor of seeing and talking to my customers,” she says. “I’m not scared of a challenge. I love to work, and I probably overdo it, but I’ve gotten to a point where this is just exhausting and demoralizing. This year has beat me down.”

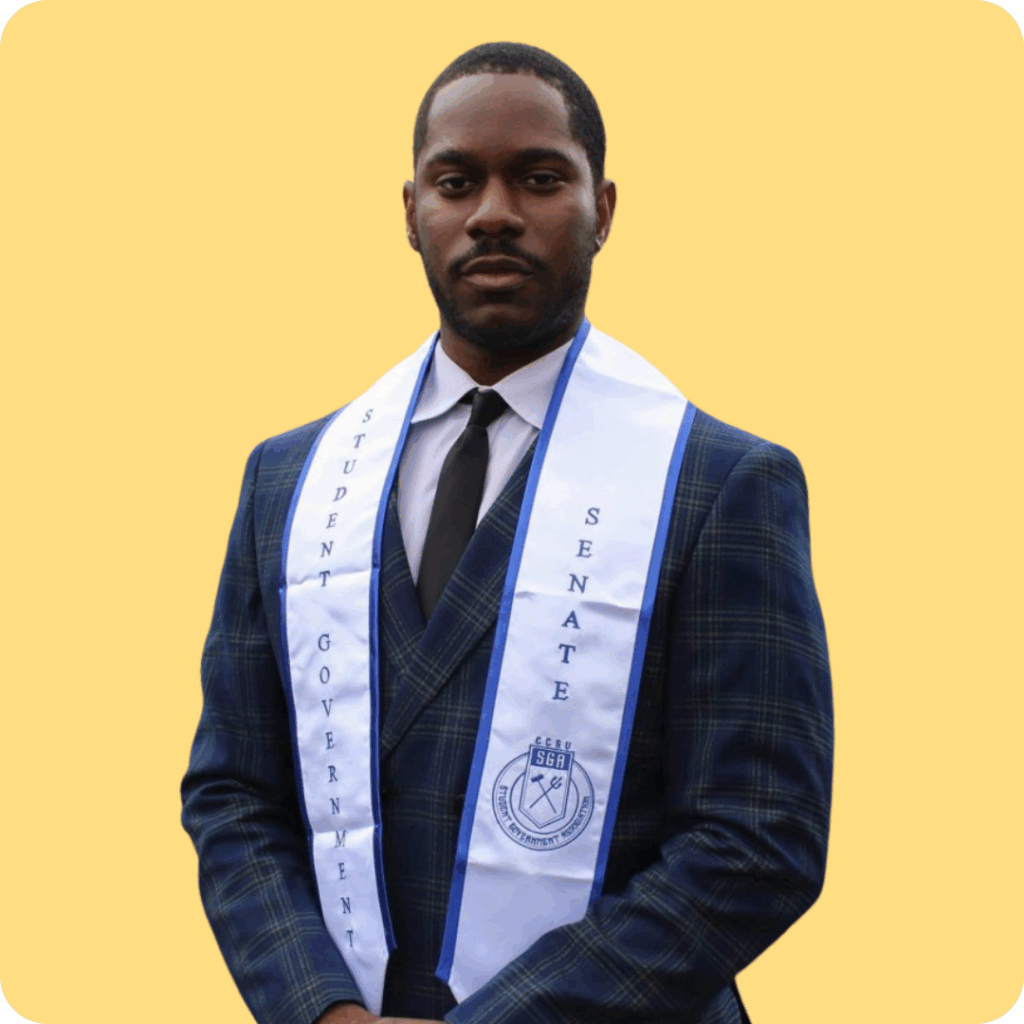

Meet Saquan Taylor, an underemployed recent college graduate

The latest statistics have also missed people like Saquan Taylor, a 27-year-old jobseeker who keeps finding that the doors to better work are all closed.

Most days for Taylor follow the same pattern: wake up at 6:45am, work a full day as head teacher at a child care facility in Connecticut, hit the gym, eat dinner — and then, for two hours, scroll through job boards. He calls LinkedIn, Handshake and Glassdoor his “social media feeds.”

Since earning his associate’s degree in 2021, he’s applied to roughly a thousand jobs. He’s landed only six interviews.

Taylor has gotten so few responses to his applications back — 20 or 30, he estimates — that he doesn’t even bother reading the emails in full anymore. He scrolls straight to the end to see a phrase that, at least so far, has always been there: “We regret to inform you that we have decided not to move forward with your application at this time.”

“People want to work. They’re just not being given the opportunity to work,” he says. “Things are booming, the stock market is great, but it’s only great for some people. If you’re not financially well, then it’s not great for you.”

Taylor studied political science and hopes to work as a department head for a government agency one day. Federal job cuts, however, have made the field more competitive.

He’s giving himself until December to find something new before moving back to New York City, where he hopes to find more opportunities. For now, he’s living at home with his mom in Connecticut, paying down bills and his student loans.

Some days, the job search feels like a test of self-worth. That’s when he’ll remind himself of where he came from: a studio apartment shared with 13 family members after moving from Jamaica to New York. His mother worked multiple jobs and became the first in their family to buy a house — a drive he’s tried to emulate.

Earlier this year, Taylor finished his bachelor’s degree, graduating with honors from Central Connecticut State University, after originally having to drop out from a four-year university in 2020 for financial reasons.

“As the years went on, I saw my mom do things I’d really consider superhuman. Once she puts her mind to something, she’s going to do it,” he says. “You have to really trick yourself into believing that there is goodness out there and hoping for the better. I try to remain humble but also hopeful that there is a better day, and I’m doing what’s necessary right now to make that day come true.”

Stay patient and cut yourself some slack, this recruiter says

Kyle Rapaport has taken it upon himself to validate what other jobseekers are experiencing. Rapaport is a recruiter for companies in the supply chain industry, the epicenter of Trump’s trade war. He spends his days trying to connect people who need jobs with companies who need workers. Lately, he feels as exhausted as the jobseekers he talks to.

Companies are pickier than ever, he says. He’s seen some firms leave roles open for a year, passing up qualified candidates in hopes of finding a perfect one who’ll check every box. Others, meanwhile, are motivated to hire one week, then a couple weeks later implement a hiring freeze after reevaluating their finances. Even in a tough market, he’s still witnessed a stigma for hiring unemployed workers.

“Companies know they are in control of the market,” he says. “It’s really tough to see candidates that I work with posting on LinkedIn, week after week, just not being able to land a position for one reason or another. I want to help them. Trying to help them and not being able to can be really frustrating and really taxing.”

Certified financial therapist Nate Astle has been starting to remind his clients that they should budget for fun in their emergency fund just as much as their necessities, knowing how much longer job searches are taking — and how emotionally challenging they can be.

“People say I have to distinguish between my needs versus wants, but wants are needs, and we need to have wants,” Astle says. “If I have been used to a certain lifestyle where I can go to the movies if I need to and suddenly I can’t, eventually I’m going to say, ‘Screw it. I’m going to do whatever I want to do because I’m so sad and depressed.’ We need to budget for that fun. It’s the most important money we spend.”

Money tip:

Financial experts typically recommend keeping at least six months’ worth of savings in an emergency fund, but any amount will help. The average unemployed worker has been jobless for more than six months, according to the latest Labor Department data.

When Rapaport can’t find someone a job, he’ll do the next best thing that he thinks will help: listen and give advice. He frequently passes along resume feedback, interview or negotiation tips and just general encouragement. His best advice to jobseekers is to leverage your network and to just stay patient.

“If you are searching for a job in this market, especially if you are unemployed, you are going to get burnt out,” he says. “There is so much rejection, and a lot of times, it’s a job that you may be perfectly qualified for, but you’ll just never hear back. Validate your own feelings, that this is very frustrating, but give yourself grace and know that you’re not alone in going through this. There are thousands of candidates, if not even more, who are experiencing the same thing every single day. It’s a matter of just continuing to fight through it.”

Why we ask for feedback

Your feedback helps us improve our content and services. It takes less than a minute to

complete.

Your responses are anonymous and will only be used for improving our website.

Help us improve our content

Read the full article here